- Published on

Dự Đoán Giá Cổ Phiếu Với Mạng LSTM

- Authors

- Name

- Kevin Nguyen

Chuẩn Bị Môi Trường

Trước khi bắt đầu, hãy đảm bảo bạn đã cài đặt các thư viện cần thiết như Pandas, Matplotlib, NumPy và TensorFlow.

import pandas as pd

import matplotlib.pyplot as plt

import numpy as np

import tensorflow as tf

from tensorflow import keras

from tensorflow.keras.models import load_model

import seaborn as sns

import os

from datetime import datetime, timedelta

import warnings

warnings.filterwarnings("ignore")

plt.style.use('fivethirtyeight')

Đọc Dữ Liệu

Về dữ liệu bạn có thể sử dụng dataset

Đầu tiên, chúng ta cần đọc dữ liệu từ tệp CSV. Chúng ta sẽ sử dụng Pandas để làm việc này.

data = pd.read_csv('VIC.csv')

print(data.shape)

print(data.sample(7))

Kích thước dữ liệu: (101266, 8)

| Ticker | Date/Time | Open | High | Low | Close | Volume | Open Interest |

|--------|------------------|------|------|------|-------|--------|---------------|

| VIC | 7/2/2020 9:34 | 90.3 | 90.3 | 90.3 | 90.3 | 250 | 0 |

| VIC | 8/5/2020 13:29 | 88.0 | 88.0 | 88.0 | 88.0 | 10 | 0 |

| VIC | 1/9/2019 9:34 | 101.4| 101.4| 100.1| 100.1 | 830 | 0 |

| VIC | 7/6/2020 11:24 | 91.4 | 91.4 | 90.6 | 90.6 | 50 | 0 |

| VIC | 12/28/2018 10:41| 102.5| 102.8| 102.5| 102.8 | 20 | 0 |

| VIC | 3/11/2020 11:06 | 96.4 | 96.5 | 96.4 | 96.4 | 2980 | 0 |

| VIC | 3/15/2019 10:14 | 118.8| 118.8| 118.7| 118.8 | 220 | 0 |

Tiền Xử Lý Dữ Liệu

Sau khi đọc dữ liệu, chúng ta cần tiền xử lý để chuẩn bị cho việc xây dựng mô hình. Các bước bao gồm chuyển đổi cột 'Date/Time' thành kiểu datetime, loại bỏ các cột không cần thiết và kiểm tra dữ liệu rỗng.

data['Date/Time'] = pd.to_datetime(data['Date/Time'])

data.info()

data = data.drop(['Open Interest'], axis=1)

data.info()

data.isnull().sum()

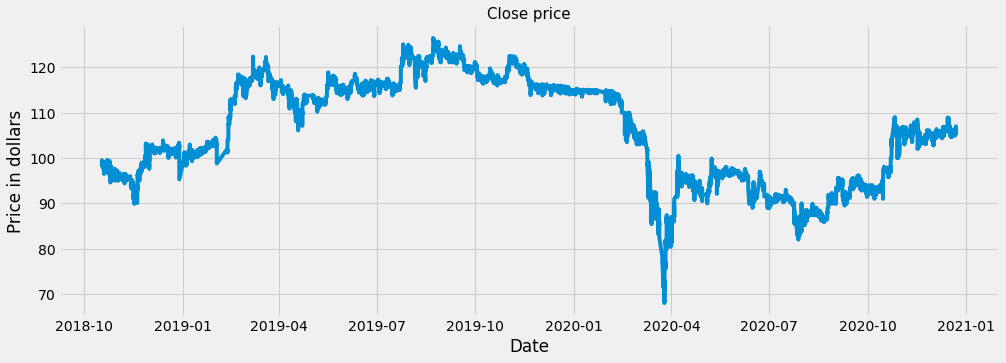

Trực Quan Hóa Dữ Liệu

Trước khi xây dựng mô hình, chúng ta nên hiểu rõ dữ liệu bằng cách trực quan hóa nó. Dưới đây là một ví dụ về cách vẽ biểu đồ giá đóng cửa.

plt.figure(figsize=(15,5))

plt.plot(data['Date/Time'], data['Close'])

plt.title('Close price', fontsize=15)

plt.xlabel('Date')

plt.ylabel('Price in dollars')

plt.show()

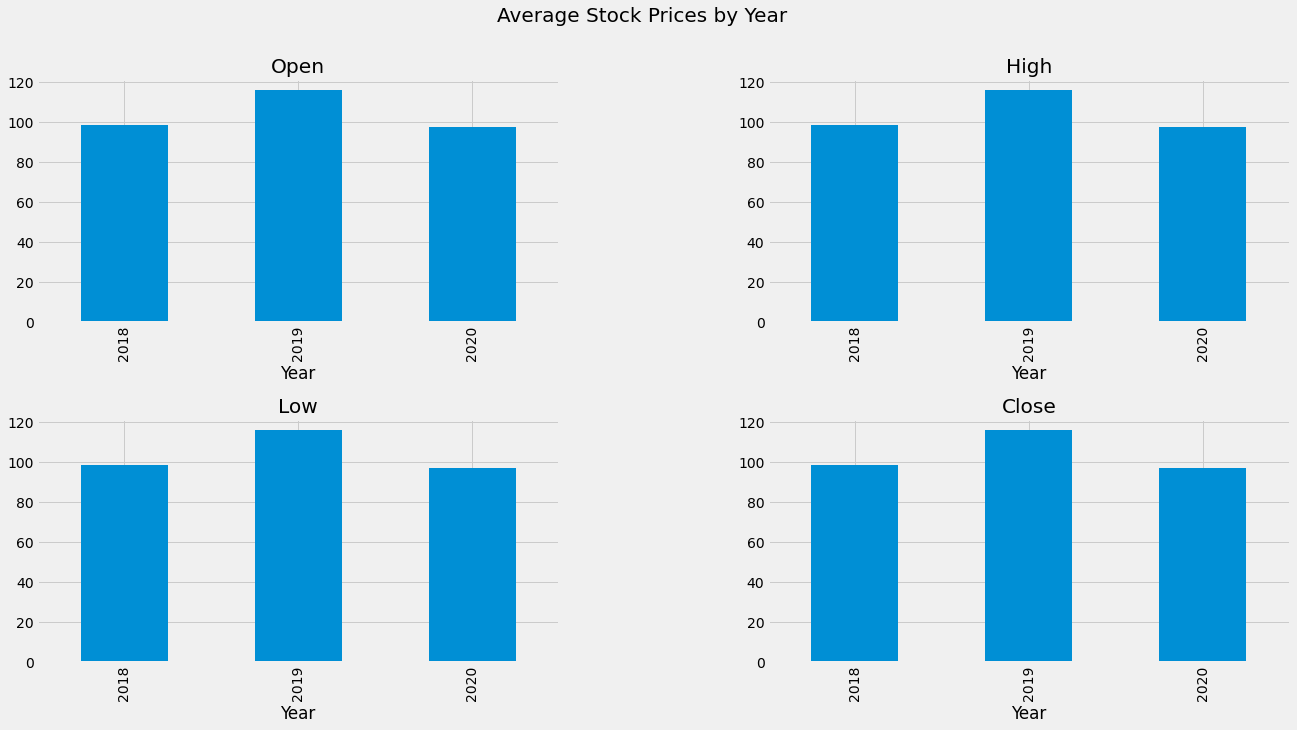

data['Year'] = data['Date/Time'].dt.year

data_grouped = data.groupby('Year').mean()

plt.subplots(figsize=(20, 10))

plt.subplots_adjust(hspace=0.4, wspace=0.4)

for i, col in enumerate(['Open', 'High', 'Low', 'Close']):

plt.subplot(2, 2, i+1)

data_grouped[col].plot.bar()

plt.title(col)

plt.suptitle('Average Stock Prices by Year', fontsize=20)

plt.show()

Tạo Bộ Dữ Liệu Huấn Luyện và Kiểm Tra

Chúng ta sẽ chia dữ liệu thành hai phần: một phần dùng để huấn luyện mô hình và một phần dùng để kiểm tra mô hình. Dữ liệu sẽ được chuẩn hóa và chia thành các chuỗi thời gian.

dataset = data['Close'].values

training = int(np.ceil(len(dataset) * .95))

print(training)

from sklearn.preprocessing import MinMaxScaler

scaler = MinMaxScaler(feature_range=(0, 1))

dataset = dataset.reshape(-1, 1)

scaled_data = scaler.fit_transform(dataset)

train_data = scaled_data[0:int(training), :]

# prepare feature and labels

x_train = []

y_train = []

for i in range(60, len(train_data)):

x_train.append(train_data[i-60:i, 0])

y_train.append(train_data[i, 0])

x_train, y_train = np.array(x_train), np.array(y_train)

x_train = np.reshape(x_train, (x_train.shape[0], x_train.shape[1], 1))

Xây Dựng Mô Hình LSTM

Mô hình LSTM sẽ giúp chúng ta dự đoán giá cổ phiếu dựa trên dữ liệu lịch sử. Mô hình sẽ có hai lớp LSTM, một lớp Dense, và một lớp Dropout.

model = keras.models.Sequential()

model.add(keras.layers.LSTM(units=64,

return_sequences=True,

input_shape=(x_train.shape[1], 1)))

model.add(keras.layers.LSTM(units=64))

model.add(keras.layers.Dense(32))

model.add(keras.layers.Dropout(0.5))

model.add(keras.layers.Dense(1))

model.summary

model.compile(optimizer='adam',

loss='mean_squared_error')

history = model.fit(x_train,

y_train,

epochs=10)

Đánh Giá Mô Hình

Chúng ta sẽ đánh giá mô hình bằng cách sử dụng sai số bình phương trung bình (MSE) và sai số bình phương trung bình căn (RMSE).

mse = np.mean(((predictions - y_test) ** 2))

rmse = np.sqrt(mse)

print("MSE:", mse)

print("RMSE:", rmse)

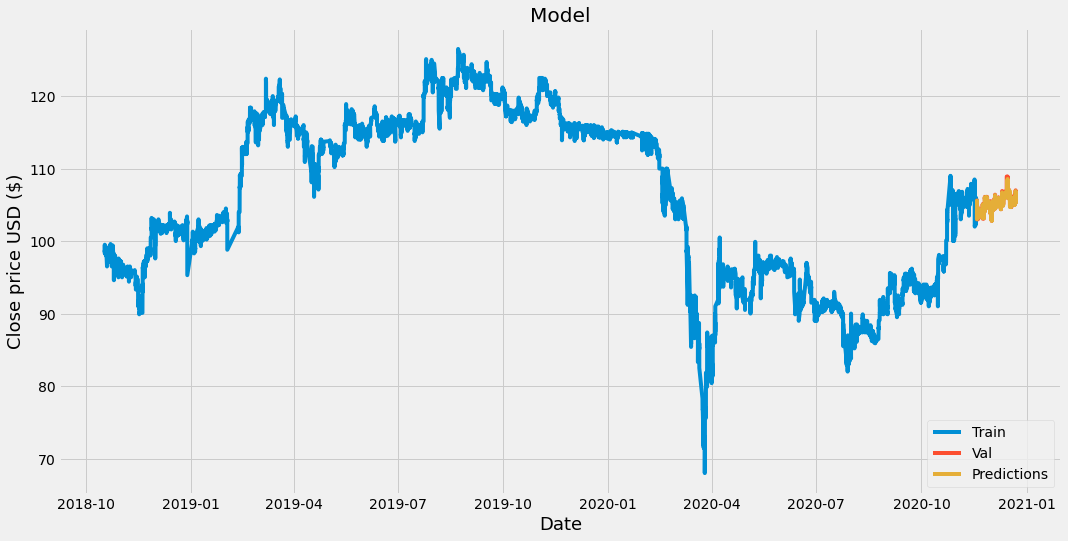

Dự đoán giá cổ phiếu trong tương lai

train = data[:training]

valid = data[training:]

valid['Predictions'] = predictions

#Visualize the data

plt.figure(figsize=(16,8))

plt.title('Model')

plt.xlabel('Date', fontsize=18)

plt.ylabel('Close price USD ($)', fontsize=18)

plt.plot(train['Date/Time'], train['Close'])

plt.plot(valid['Date/Time'], valid['Close'])

plt.plot(valid['Date/Time'], valid['Predictions'])

plt.legend(['Train', 'Val', 'Predictions'], loc='lower right')

plt.show()

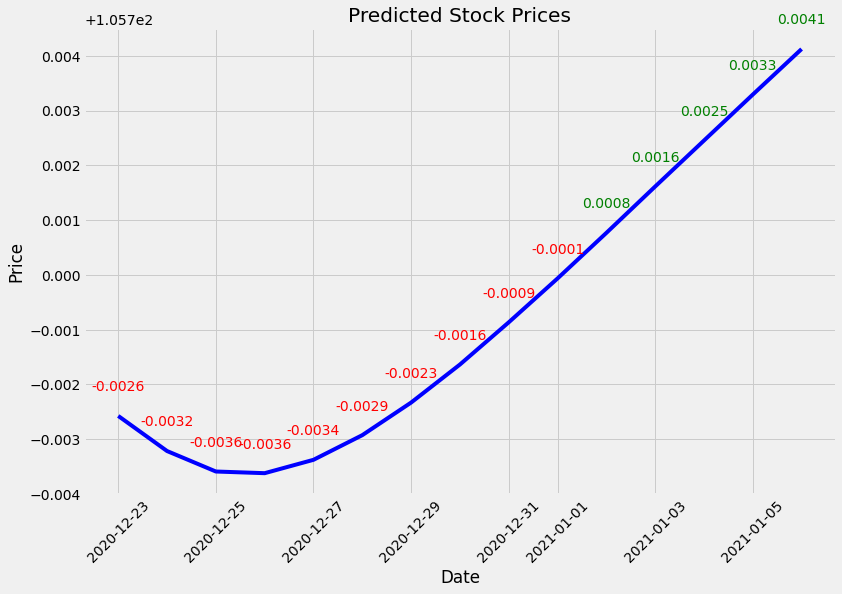

Date Price Change

0 2020-12-23 105.697426 -0.002574

1 2020-12-24 105.696785 -0.003215

2 2020-12-25 105.696411 -0.003589

3 2020-12-26 105.696381 -0.003619

4 2020-12-27 105.696625 -0.003375

5 2020-12-28 105.697075 -0.002925

6 2020-12-29 105.697670 -0.002330

7 2020-12-30 105.698364 -0.001636

8 2020-12-31 105.699135 -0.000865

9 2021-01-01 105.699936 -0.000064

10 2021-01-02 105.700768 0.000768

11 2021-01-03 105.701614 0.001614

12 2021-01-04 105.702454 0.002454

13 2021-01-05 105.703293 0.003293

14 2021-01-06 105.704124 0.004124

Bạn có thể tìm full code ở đây Colab